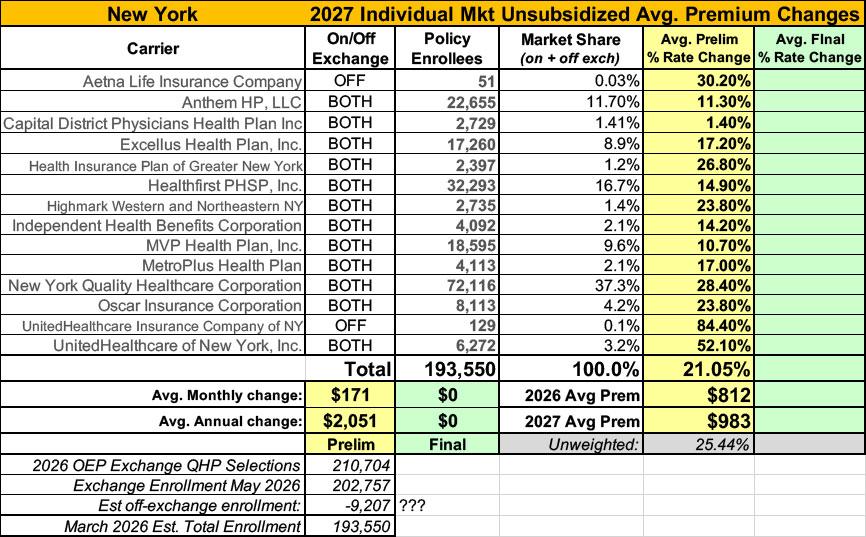

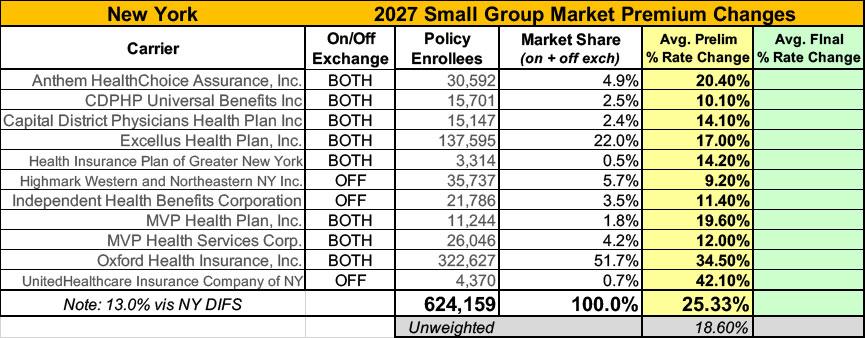

2027 Rate Changes - New York: +21.1% indy, +25.3% sm. group (preliminary)

Fri, 06/12/2026 - 1:06pm

via the New York Dept. of Financial Services:

Health insurers must make an application to the Department of Financial Services to evaluate their proposed rate changes. The Department reviews the rate applications along with the insurer’s underlying calculations to make sure that rate increases are justified and not excessive. During review, DFS may request more information from the insurer and consider comments from policyholders or the public. Rate applications and all documents relating to an application can be found here:

Individual and Small Group Medical Premium Rates

Beginning with rate application filings submitted in 2023 for benefit year 2024, rate information will be contained in one place for all insurers, separated by Market Segment.

AETNA LIFE:

Aetna is filing revisions to premium rates for Individual Conversion policies that will be sold in New York during 2027. The rates in this filing will apply to Individual Conversion policies that are renewed or sold at policy anniversary beginning on January 1, 2027. These rate changes will impact approximately 30 subscribers and 51 members.

The requested rate changes for Aetna's Individual Conversion policies are directly related to two main drivers: the overall rising cost of health care services in New York, and an adjustment to reflect changes in the type and quantity of medical services used by our members which results in increased claim expenses.

ANTHEM HP:

II. FACTORS CONTRIBUTING TO THE PROPOSED RATE INCREASE

Escalating Health Care Costs

The cost of health care services and equipment continues to be the primary reason for rate increases. A report by Mercer shows health care cost grew by 6.0% in 2025 and projects a sharper increase of 6.7% for 2026, the highest in 15 years.

Health care cost and spending trends reflect underlying changes in the demographics and health status of America’s population. The aging population is driving some of the increase – as people age, they typically utilize more health services. Between 2010 and 2050, the population aged 65 and older is expected to double, as the “baby boomer” population ages and life expectancy continues to rise2 . Indeed, the first baby boomers have now turned seventy and the percentage of workers over 65 is greater than at any period in history. As this population ages it will correspond to a further escalation of costs. Moreover, the country’s general declining health and the increase in obesity and other health concerns, even at younger ages, forces average costs upward.

Hospital

Hospitals (inpatient and outpatient care) account for the largest share of the health care premium dollar in New York, a percentage that continues to grow. Factors driving this growth include increasing demand for care, rising costs to hospitals of the goods and services needed to provide care, and the growing intensity of care needs.Prescription Drugs

Specialty drugs account for one of the biggest health benefit cost drivers. A report by Mercer explains that in 2025, the drug benefit cost per employee rose 9.4%. Additionally, specialty drug trends are expected to increase as more breakthrough gene and cellular products enter the market. 3American Rescue Plan Act and 1332 Waiver

The 2027 rate filing reflects the expected impact to the health of the ACA risk pool as well as the financial and membership impacts due to both the expiration of the enhanced ACA premium tax credits under the American Rescue Plan Act as well as the repeal of the 1332 waiver and loss of Medicaid eligibility for certain populations.

Capital District Physicians’ Health Plan:

CDPHP has filed a request for approval to the New York State Department of Financial Services for a change to the premium for this product effective January 1, 2027. Policyholders will receive rate adjustments upon their renewal in 2027. The weighted average premium adjustment is 1.4%. 2,729 members and 1,881 policyholders are affected by this request.

What’s Driving Cost Increases?

While CDPHP and our competitors continue to operate in a challenging and volatile health insurance environment, we are encouraged by meaningful improvement after multiple years of net losses. However, headwinds remain – particularly the disproportionate impact of the Medicare Wage Index on regional, not for profit plans in Upstate New York, along with rising prescription drug and hospital costs, and increasing taxes, fees, and mandates. These realities require continued discipline and focus.

What is CDPHP Doing About It?

To manage rising costs, CDPHP is taking a thoughtful and strategic approach to reducing administrative expenses while maintaining our high standards of service. This includes implementing process improvements, technology enhancements, and operational efficiencies to focus resources where they matter most – delivering value to our members. We’re also taking strategic steps to strengthen our organization through a proposed merger with Excellus Health Plan, Inc., providing important economies of scale and operational efficiencies.

Excellus Health Plan, dba Excellus BlueCross BlueShield • Univeral Healthcare

FACTORS CONTRIBUTING TO THE PROPOSED RATE INCREASE

Escalating health care costs

The cost of health care services, equipment and products continues to be the primary reason for rate increases. In 2025, the health plan overall spent nearly $7 billion on medical and pharmacy claims, or about $19 million daily.Medical cost “trend” is a very important consideration in determining the need for a premium rate adjustment. This “trend” is the anticipated change in the cost to treat patients year over year. Upstate New York is not immune to national trends in health care costs given our state’s population and demographics. The trend forecast below takes into account projected increases in costs attributed to what Excellus Health Plan pays out in claims expenses for hospital inpatient and outpatient care, professional services, pharmacy benefits, and other goods and services. The health plan’s anticipated changes in annualized medical benefit spending are summarized as follows:

- Hospital inpatient, small group: 8.1% / individual: 7.2%

- Hospital outpatient, small group: 11.4% / individual: 14.9%

- Professional services, small group: 6.5% / individual: 6.8%

- Pharmacy, small group: 9.0% / individual: 15.0%, including:

- Specialty Rx, small group: 15.0% / individual: 26.2%

- Other medical goods and services, small group: 6.9% / individual: 9.9%

Rising drug prices are having a significant impact on overall medical spending trends. Substantial savings have been achieved over the years with broad acceptance of competitively manufactured generic medicines. However, the savings trend associated with generics is being eclipsed by another trend around the rising cost and utilization of specialty medications including biologics. Every year more and more highly complex specialty medications are approved by the FDA to treat both rare and sometimes more common diseases. Specialty medications are used by approximately 2 percent of our members, but they account for more than 50 percent of total drug spend. Drug trend is a result of both increased utilization and increased unit cost.

Local hospital systems have been challenged financially due to both economic inflationary pressures as well as staffing shortages. Excellus Health Plan has responded to these provider challenges through additional contractual cost increases for our provider systems, resulting in more spending for hospital services. The impact for drug rebate credits and non-system claims’ trends is applied to the base tren

Health Insurance Plan of Greater New York (HIP):

Why do we need to change premiums?

We change premiums due to the rise in the cost of medical care, including the costs of hospital stays, prescription drugs, and other health services. Most of your premium goes toward paying for medical and pharmacy claims for members. In fact, New York State requires that at least 82% of the premium you pay directly covers member medical costs. As the cost and use of pharmacy drugs and medical services go up, so does the cost of medical care we must pay for.

HealthFirst:

Healthfirst is applying for a rate adjustment to account for marketplace trends and to reflect actual and anticipated claims costs. While several market forces continue to drive health care costs higher more generally, Healthfirst continues to strengthen the effectiveness of its care management and quality improvement programs and robust network.

Healthfirst is requesting a higher rate for 2027 because several market forces continue to drive health care costs higher. These forces include:

- Cost and utilization increases for inpatient hospital, outpatient hospital, and physician services of approximately 7%.

- Cost and utilization increases for prescription drugs, including the increased use of expensive specialty prescriptions of approximately 20%.

Healthfirst has requested an average rate increase of 14.9% for Region 4, which is composed of the five counties of New York City (Bronx, Kings, New York, Queens, Richmond), Rockland County, and Westchester County and for Region 8, which comprises Long Island (Nassau County and Suffolk County)

Highmark Western and Northeastern New York

Over the past three years, the company has incurred approximately $30 million in losses in the individual market. More than 90 cents of every premium dollar—exceeding the state-mandated medical loss ratio—is used to reimburse doctors and hospitals for members’ medical care. This emphasizes the necessity of premium rates that accurately reflect the cost of care.

Despite sustained cost pressures, our stability as a not-for-profit health plan—supported by the strength of Highmark Health—allows us to leverage shared innovation and strategic partnerships to improve efficiency and help mitigate the extent of the proposed 2027 rate increases.

This rate change application affects only the members enrolled in community-rated products for individuals. Based on current membership numbers, we estimate that 2,735 members will be affected by the rate change.

Based on the reasons explained above, we are requesting that the Department of Financial Services grant our submitted premium rate increase of 23.8% for its community-rated individual products to take effect on January 1, 2027. This increase is primarily due to cost and utilization increases.

Independent Health Benefits Corporation

Premium rates tend to rise each year because of the normal inflation of healthcare claim costs. Moreover, in addition to cost increases, utilization of healthcare services also tends to rise as new technologies, services, and prescription drugs are introduced to the marketplace.

For 2027, IHBC is projecting an overall claim expense trend of 14.7%. All else being equal, this would require a corresponding premium rate increase to keep pace with costs. However, because of other factors, IHBC is requesting a rate change lower than the overall claim expense trend.

MVP Health Plan, Inc.

Premium rates are changing due to the following reasons:

- The rising cost and utilization of medical services and prescription drugs (+10.1%)

- A change in claim projection from the prior year which includes the impact of changes in anticipated payments/receipts in the Federal Risk Adjustment Program (-0.7%)

- A change in non-claim expense items including taxes and fees (+1.3%)

MetroPlus Health Plan, Inc.

We are proposing a 17.0% weighted average increase for CY 2027 per member per month premium rates effective 1/1/2027. The rate increase will vary across plans, ranging from 13.7% to 27.3%. The increase will affect 4,113 members (3,614 policyholders). The primary drivers of increases are:

- Emerging experience (including risk adjustment, member mix impacts, and Essential Plan members returning to QHPs): 2.8%

- Trends due to higher utilization of health care services, higher payments to health care providers, and higher prescription drug costs: 11.3%

- Residual impacts of the American Rescue Plan Act subsidies ending: 0.7%

- Administrative cost change: -2.3%

- Benefits and AV changes: 3.9%

New York Quality Healthcare Corporation (Fidelis)

Fidelis Care’s rate filing is driven by seven primary considerations:

- Adjustment from actual to expected experience

- Anticipated higher medical and pharmacy costs and increased use of services by our members

- Risk Adjustment transfer payment that considers the level of illness of our members

- Updates to statewide average morbidity assumptions reflecting population health risk

- Changes in prescription drug regulations

- The impact of the return of 200–250% FPL members from EP plans to the Individual Market

- Changes in the age and gender of those we cover as well as their level of health and wellness

Oscar Insurance:

Why are premiums going up?

We never base premiums on your age, gender, or health. There are two main reasons for higher premiums: prices for drugs and health care services are on the rise, and members are projected to use more care. When our costs go up, we unfortunately have to raise premiums, as do all other carriers. We expect to pay at least $0.85 of every $1 we collect in premiums towards our members’ medical care, and sometimes we pay even more than that. We use whatever is left to cover the cost of running our business.

United Healthcare Insurance Company of New York, Inc.

A part of the medical costs includes a pooling technique established under the Affordable Care Act (ACA) called Federal Risk Adjustment. This attempts to equalize risk within the New York Individual market and requires carriers to set rates at the statewide average risk level. The estimated risk adjustment value reduces the costs by 26.4% percent.

We have increased the index rate by 0.3% to account for the impact of legislative changes to Behavioral Health Network Adequacy. A rate impact of 0.8% is added for costs associated with the Independent Dispute Resolution process, including both the federal program and additional New York-specific requirements. Additionally, a 2.3% rate impact is attributed expanded coverage for certain prescription drug therapies (including medically necessary GLP-1 medications).

To account for uncertainty related to economic and supply chain conditions and their impact on medical costs, particularly pharmaceuticals, a total price impact of 0.9% is included in the initially submitted rate filing. This estimate may be updated as additional information becomes available. An adjustment of 0.5% was applied to account for the impact of the new proposed premium tax being considered in the NYS Budget.

The impact of the expiration of the American Rescue Plan Act expanded subsidies and the CMS Marketplace Integrity and Affordability Proposed Rule account for 12.7% of the requested rate change.

The requested rate changes also include the impacts of plan relativity changes due to pricing model updates (rate increases or decreases depending on the plan) and benefit changes (rate neutral, increases or decreases depending on the plan). Specific information regarding the benefit changes will be communicated separately to those in impacted plans.

Put them all together and it's not a pretty picture: The weighted average preliminary 2027 rate hikes for the individual market come in at around 21.1% (although NY DFS actually puts it slightly lower, at 20.7% for some reason).

Meanwhile, New York's small group market carriers are requesting weighted average increases of 25.3% (in this case, NY DFS puts the average slightly higher, at 25.7%).

It's also worth noting that the total enrollment as of spring 2026 including off-exchange enrollees totals less than 194,000 people...even though the official NY State of Health enrollment report puts on-exchange enrollment only as of May 2026 at ~203,000. The only way that makes sense is if if there was a sudden surge in enrollment from March (the as of date most carriers use in their filings) until May...except the NYSoH reports for March & April are also over 200,000, so I'm not sure what to make of the discrepancy.

As a couple of the carrier filings reference, enrollment in the NY ACA exchange market is expected to spike starting in July as up to a whopping ~450,000 New Yorkers are kicked off of the state's Basic Health Plan (BHP) Program due to the GOP's so-called "One Big Beautiful Bill Act," which will also result in a small portion of them becoming eligible for subsidized exchange enrollment instead...which will have a significant impact on the exchange market risk pool.

Advertisement